If cash keeps landing after payroll, you don’t have a profit problem, you have a timing problem. The Cash Conversion Cycle shows how many days cash is tied up between doing the work and getting paid. Below, we’ll explain CCC in plain English, give you a mini-calculator, and show five quick plays to shorten your cycle.

Who this is for: UK service-based SMEs (5–30+ staff), consultancies, agencies, IT/MSPs, professional services, who invoice B2B on terms.

What is the Cash Conversion Cycle (CCC)?

CCC is the number of days your cash is tied up in operations before you get it back.

Formula:

CCC = DIO + DSO − DPO (Days Inventory Outstanding + Days Sales Outstanding − Days Payables Outstanding). Investopedia

Service-business note: If you carry no inventory, treat CCC ≈ DSO − DPO. If you run work-in-progress (WIP) (unbilled time/projects), WIP is treated like inventory under UK GAAP (FRS 102), so include it in DIO. ICAEW

Why CCC matters: Lower CCC = fewer crunches, less borrowing, and more strategic freedom.

Don’t assume readers know the acronyms (quick glossary)

- DSO (Days Sales Outstanding): average time customers take to pay.

- DIO (Days Inventory Outstanding): how long stock/WIP sits before billing.

- DPO (Days Payables Outstanding): how long you take to pay suppliers.

- WIP (Work in Progress): costs/time on unbilled work counted within inventories under FRS 102. ICAEW

How to calculate DSO, DIO and DPO (plain-English formulas)

- DSO: (Average Accounts Receivable ÷ Credit Sales) × 365

- DIO: (Average Inventory or WIP ÷ Cost of Sales) × 365

- DPO: (Accounts Payable ÷ Cost of Sales) × 365

These are the standard definitions you’ll see in finance texts and training materials. Corporate Finance Institute

Related reading inside Heights:

• Core finance formulas you’ll reuse

• Reduce debtor days (DSO)

• Supplier terms done right (DPO)

• WIP: when and how it counts under UK GAAP

Map your Order-to-Cash (O2C) to find the delays

Sketch your real-world path: Proposal → PO/engagement → Delivery (timesheets/milestones) → Invoice (same day!) → Reminders → Payment → Allocation. Add timestamps to find where days leak (waiting for a PO, late milestone sign-off, slow invoice runs, no payment link, disputes, etc.).

Heights Tip: Before signing a big client, check their payment behaviour on the government’s Payment Practices Reporting service, see average days to pay and % paid late. (Great for negotiating deposits/terms.) GOV.UK

Five quick plays to shorten your CCC

- Invoice earlier (and more often). Switch scope to deposit + milestones so WIP becomes billable sooner.

- Make paying effortless. Add Direct Debit/card links to every invoice and automate reminders (day 3, 7, 14, 21).

- Use your lawful late-payment tools (B2B). UK law lets you charge statutory interest (8% + Bank of England base rate) and fixed-sum compensation on overdue business-to-business invoices, use the official calculator to work it out. GOV.UK

- Qualify “slow payers” up front. Use the Payment Practices Reporting service when bidding or renewing. GOV.UK

- Align supplier terms (DPO) to receipts, fairly. Aim to pay on or just after your typical receipt day, without breaching contracts or harming relationships.

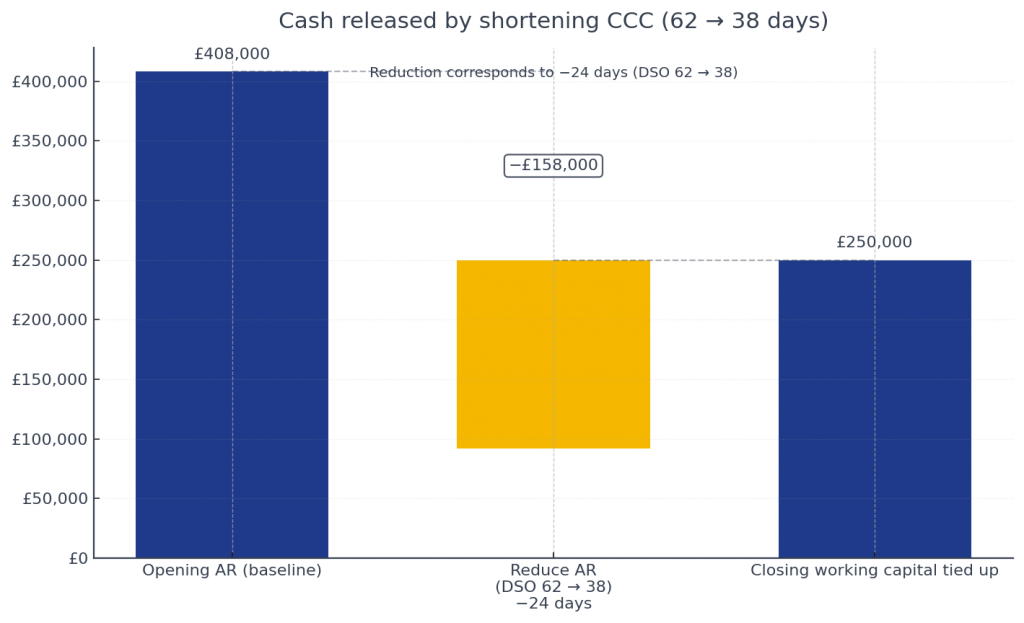

Worked example (service SME): CCC 62 → 38 days and the £ impact

Business: £2.4m revenue (£200k/month), service firm with minimal physical stock.

Baseline (service mode):

- DSO = 62 days (AR ≈ £408k on £2.4m revenue)

- DIO = 0 (treating WIP as negligible to start)

- DPO = 0 (neutral for illustration)

- CCC = 62 days

Interventions (90 days):

- Deposit + weekly milestone billing (so you invoice earlier)

- Direct Debit on onboarding + automated reminders

- PO discipline (no PO → no work) and same-day invoicing

After:

- DSO = 38 days

- DIO = 0 (WIP kept near zero by weekly billing)

- DPO = 0 (held neutral for clean comparison)

- CCC = 38 days

£ impact: Daily Sales ≈ £6,575. A 24-day CCC reduction releases ~£158k of cash (24 × £6,575) from your working capital.

You can also show this via working-capital balances: AR falls from ~£408k to ~£250k (cash released ≈ £158k).

(If you do carry WIP, include it in DIO. Under FRS 102, contract WIP is presented within inventories, so eliminating WIP accelerates both DIO and CCC.) BDO

Tiny calculator: DSO/DIO/DPO → CCC

Cash Conversion Cycle calculator

Frequently asked (in plain English)

What is a “good” CCC for a service SME?

There’s no one UK number. Track and improve your own trend each quarter. Aim to keep WIP near zero, DSO ≤ 30–35 days, and DPO aligned to when cash typically arrives (without breaching supplier terms). (General finance practice; use your own baseline as the benchmark.) Corporate Finance Institute

Can I charge late-payment interest to other businesses?

Yes, for B2B you can charge statutory interest (8% + Bank of England base rate) and a fixed-sum compensation per invoice unless your contract sets something else. GOV.UK explains the rules and provides links to current base rates; you can also use the official calculator. GOV.UK

How do I check if a big customer pays on time?

Use the government’s Payment Practices Reporting service to see average days to pay and the % paid late for large UK businesses. GOV.UK

Does CCC apply if I have no stock?

Yes, treat CCC as DSO − DPO. If you hold WIP, include it in DIO because WIP is part of inventories under FRS 102. ICAEW

What to do next

- Download the 52-week rolling forecast (free). (Plan receipts vs payments and pressure-test your CCC targets.)

- Book a 20-minute planning call to map your O2C, set a 90-day DSO target, and agree the chasing rhythm.